Wholesale Inflation Falls Again; #Disinflation Station

Wholesale Inflation Falls Again; #Disinflation Station

Preface

The Producer Price Index (PPI), as opposed to Consumer Price Index (CPI) that we received yesterday, came in below estimates both for headline and core.

In fact, overall PPI MoM has come in negative for two consecutive quarters - that’s not disinflation, that’s deflation.

Core CPI MoM has come in at 0% for the last three months.

Here is a chart of Core PPI:

")

Parts of PPI lead directly into the inflation index called PCE and Core PCE), and its those two that are the Fed’s preferred measures of inflation.

PCE (and Core PCE) came in below estimates for November and signs now point to the same for December (the report is out in January).

The consensus for PCE and Core PCE YoY measures for the month of Dec are 2.7% and 3.0%, respectively and then drop to 2.3% and 2.7% respectively, for January.

Those January numbers would mean that the Fed has, for all intents and purposes, hit its 2% target.

CPI has some essentially broken computation methodologies and that will take a while longer to get to 2%, but the Fed’s (rightly) preferred measure, is about to hit target.

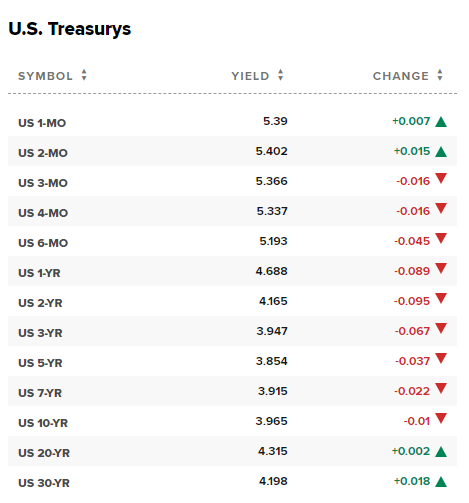

With the news rates have dropped again:

And ever further, the 2yr / 10yr inversion is getting close to ending.

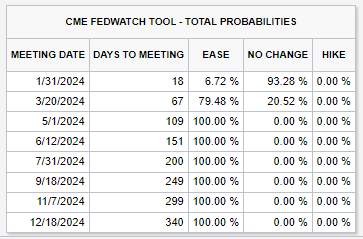

Further yet, the probability of a rate cut in the March Fed meeting has risen back to almost 80% and is at 100% for May:

That’s it for today!

Data Lede

Producer Inflation (PPI YoY):

1% vs 1.3% consensus and 0.8% prior.

Producer Inflation (PPI MoM):

-0.1% vs 0.1% consensus and -0.1% prior.

Producer Core Inflation (PPI YoY):

1.8% vs 1.9% consensus and 2% prior.

Producer Core Inflation (PPI MoM):

0% vs 0.2% consensus and 0% prior.

Context and Charts - Producer Inflation (PPI YoY)

Producer Inflation (PPI YoY) is 1%, with 1.3% consensus estimates, and 0.8% in the prior month.

In the United States, the Producer Price Index for final demand measures price change for commodities sold for personal consumption, capital investment, government, and export.

This is one of three inflation indices that the Fed tracks; the other two being CPI and PCE.

Producer Inflation (PPI YoY) 10-Year chart (Source)

")

Context and Charts - Producer Inflation (PPI MoM)

- US producer prices declined 0.1% month-over-month in December 2023, matching the decrease in November and defying forecasts of a 0.1% rise.

- Goods cost fell by 0.4%, marking the third consecutive decline, primarily due to a 12.4% drop in diesel fuel prices, while gasoline prices increased by 2.1%.

- Service prices remained unchanged, consistent with the previous two months. Notably, costs for securities brokerage, dealing, and investment advice rose by 3.3%, but margins for machinery and vehicle wholesaling fell by 5.5%.

- Core Producer Price Index (PPI), which excludes food and energy, was also flat, continuing the trend from the past two months and falling below the anticipated 0.2% increase.

- Year-on-year, the headline PPI rate slightly increased to 1% from 0.8%, lower than the expected 1.3%. Meanwhile, the core rate decreased to 1.8% from 2%, below the forecasted 1.9%.

Producer Inflation (PPI MoM) 18-Month chart (Source)

")

Context and Charts - Producer Core Inflation (PPI YoY)

Producer Core Inflation (PPI YoY) is 1.8%, with 1.9% consensus estimates, and 2% in the prior month.

This is the PPI excluding food and energy.

Producer Core Inflation (PPI YoY) 10-Year chart (Source)

Context and Charts - Producer Core Inflation (PPI MoM)

- In the United States, Core Producer Prices, excluding food and energy, remained steady for the third consecutive month in December 2023, maintaining the same rate as in November and October, contrary to market predictions of a 0.2% increase.

- Annually, the US core Producer Price Index (PPI) experienced a 1.8% rise in December, a slowdown from the 2% growth seen in the previous month, and was lower than the anticipated 0.9% increase.

This is the PPI MoM excluding food and energy.

Producer Core Inflation (PPI MoM) 18-Month chart (Source)

")

Thanks for reading. Please do share this post if you find it helpful.