Wage Growth Drops to 2-year Low; Payrolls Strong; Revisions Shake Amateurs

Wage Growth Drops to 2-year Low; Payrolls Strong; Revisions Shake Amateurs

Preface

Today we received the non farm payrolls (NFP) report (the “jobs report”) for February as well a revisions to the prior months.

The real headline was the wage growth number that came in well below estimates at 0.1% month over month (MoM) versus estimates of 0.3% and last month’s 0.4%, which was revised down from the initial reading of 0.5%.

It was the smallest gain in wages since February 2022.

That’s crazy that January seemed so hot and then was revised lower and now February dropped to a two-year low.

Here is a chart:

US Average Hourly Earnings YoY 10-Year chart (Source)

Crazy right. Or… hold that thought for one sec. Let’s look at jobs first:

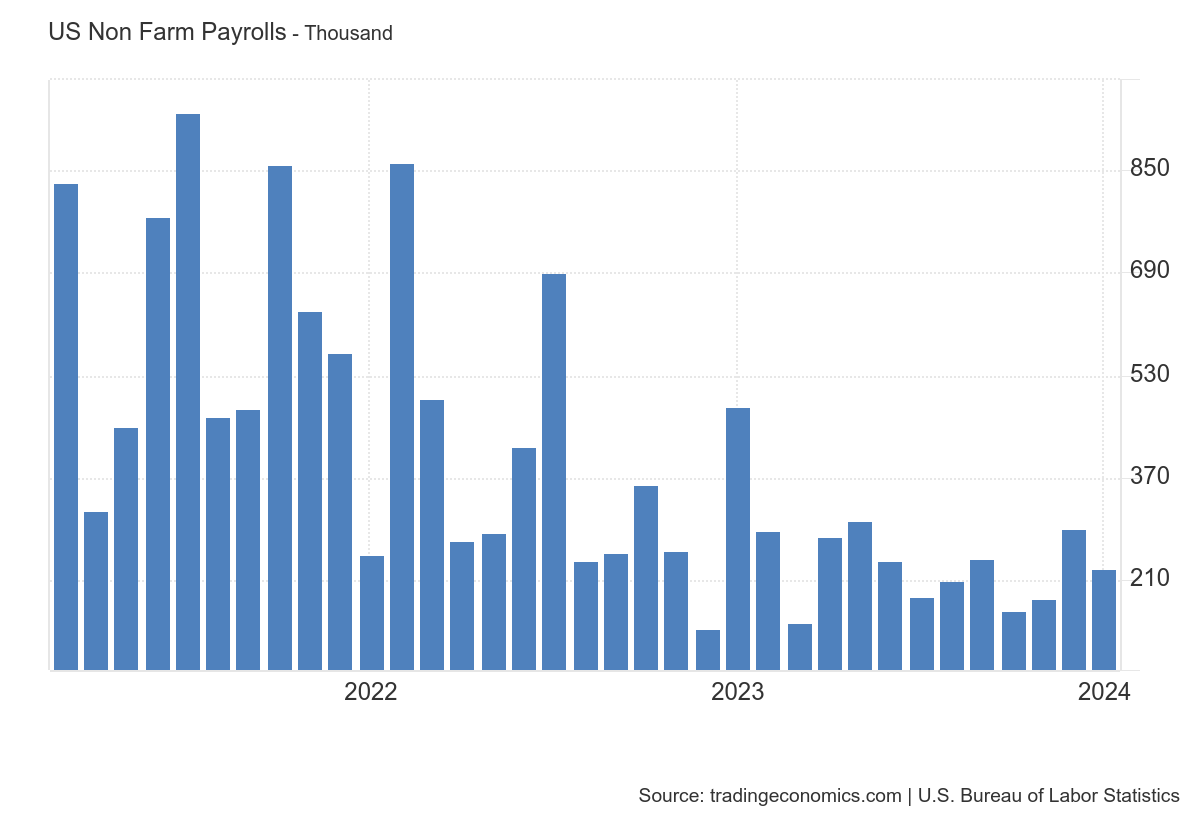

February payrolls came in strong at 275K new jobs versus expectations for 200K.

But as we suspected January (last month) was revised down massively by 124K jobs and Dec, too, was revised down by 43K jobs. Here is a chart:

So, January 2024 now reads 229K, revised down from the “hair on fire, world is on fire, inflation is on fire, the world is ending, Fed will never cut” 353K initially reported.

Oops!

The somewhat hysterical rection to the blockbuster (at first) January NFP report is yet another reminder of how many people don’t understand economic data yet insist on commenting on it.

While everyone having a voice is the pillar to democracy when it comes to who represents us in government and what they enact into law, “democratizing” economic or financial analysis leads to people simply getting dumber.

In that same vein, John and Jane Doe performing surgery would 'democratize' surgery, but it it would also kill people. Let’s not kill people… or get dumber.

The number of domain experts grows very slowly (in any field) while number of amateurs grows exponentially (thanks Twitter + ChatGPT!), and the result is a watered down narrative which is a fancy phrase for worse.

So, we’ll repeat the exact words we wrote when the Jan 2024 NFP report came out last month, which were the exact words we wrote in February 2023 when the Jan 2023 NFP report came out:

In total, wage inflation has stalled, is consistent with 2% inflation (the Fed’s target), was the lowest in two-years, all while the job market remains robust but not overheating.

While we’re here, I’ll point out that there will be revisions to this data as well and Feb, too, has a tendency to be a little “off.”

You will also read commentary on the unemployment rate rising from 3.7% to 3.9%, but on a month to month basis the change in that number often not statistically significant. So, the world is ending again, until it isn’t. Don’t worry, the Twitter posts are coming.

Nick Timiraos notes that the index of aggregate weekly payrolls for private-sector workers, which measures the total earnings of employees in the private sector, reflecting changes in both employment levels (jobs) and wage growth (inflation), was up 5.3% over the last 12 months and looks like this over the last year:”

Inflation is over.

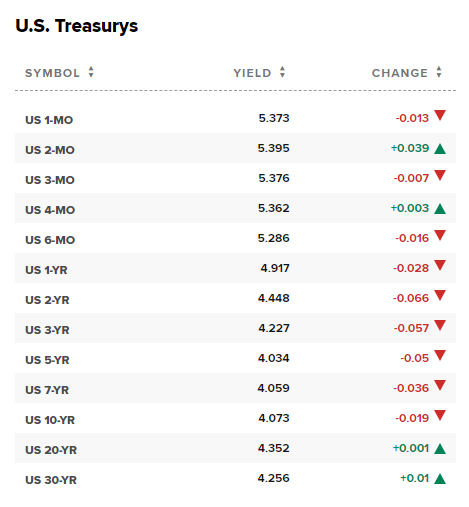

Treasury yields are down a little - let’s call it nearly unchanged:

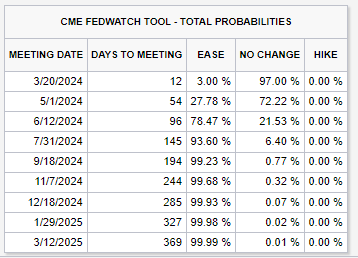

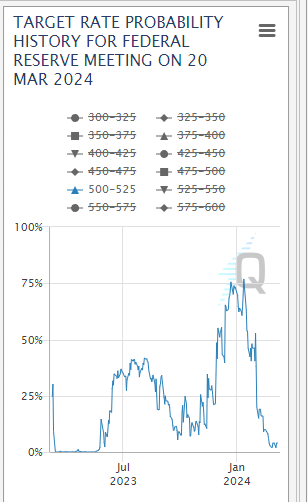

The probability of a Fed rate cut has moved to ~28% in May and now ~78% in June.

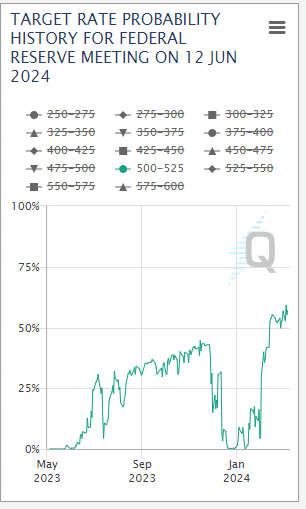

Here is how that June probability has moved over time:

But, here is how that March probability has moved over time too:

The futures markets are both a reflection of a probability and a reflection of speculative and hedging positions so the numbers will move both based on economic data but also on asset manager and dealer positioning.

Basically the futures market has taken those high odds of a rate cut in March off the table and moved that probability into June.

And what do I think?

I think that what the Fed thinks about inflation is the “only” thing that matters which is a far worse place than I believed we were one year ago: which was just the first part of that statement when I thought it was inflation in and of itself that was the only thing that mattered.

I have changed my mind: inflation doesn’t matter, it’s only what the Fed thinks about inflation that matters.

That’s a worse place to be because it implies that we are not dependent on good (lower) inflation data, we are dependent on the Fed accepting good (lower) inflation data.

That ain’t gonna be easy and feels a lot like I said it did a month ago: F*** around and find out.

Still, the data today is very good for the soft landing crew.

Data Lede

US Non Farm Payrolls:

275K vs 200K consensus and 229K prior.

US Average Hourly Earnings YoY:

4.3% vs 4.4% consensus and 4.4% prior.

US Average Hourly Earnings MoM:

0.1% vs 0.3% consensus and 0.5% prior.

US Average Weekly Hours:

34.3 vs 34.3 consensus and 34.2 prior.

US Unemployment Rate:

3.9% vs 3.7% consensus and 3.7% prior.

US Labor Force Participation Rate:

62.5% and 62.5% prior.

Conclusion

If you want more like this with a discussion about a portfolio of technology comanies (stocks) with an auditor verified track record dating back to 2016, checkout CML Pro.