Today: Inconceivably Good; How is This Possible?

Today: Inconceivably Good; How is This Possible?

Lede

For now, a moment in time, this is one of the most inconceivably good economic outcomes that could have been dreamed up:

A booming GDP, booming employment, growing real wages, and plummeting inflation.

Today we received PCE and Core PCE inflation measures for November and inflation was softer than expected, again.

At the same time, personal income grew nicely and inline with estimates while personal spending came in a bit below estimates but still grew.

Yesterday we learned that the final numbers for Q3 2023 were lower than estimates and that momentum continues to roll into Q4.

Recall that yesterdays Q3 data showed Core PCE Inflation exactly at the Fed's target (2%) while GDP growth was the highest in 6-quarters.

Here is today’s data (for November):

PCE Price Inflation YoY:

2.6% vs 2.8% consensus and 2.9% prior.

PCE Price Inflation MoM:

-0.1% vs 0% consensus and 0% prior.

Core PCE Price Inflation YoY:

3.2% vs 3.3% consensus and 3.4% prior.

Core PCE Price Inflation MoM:

0.1% vs 0.2% consensus and 0.1% prior.

US Personal Income MoM:

0.4% vs 0.4% consensus and 0.3% prior.

US Personal Spending MoM:

0.2% vs 0.3% consensus and 0.1% prior.

How Can This Be Happening!?

An irritant was introduced in 2020: COVID.

That irritant wreaked havoc on our collective (and personal) health and psyches. It also wreaked havoc on our economy - jobs, inflation, GDP.

But the further we get from the irritant, the less irritated we are.

The economy has recovered beautifully. Inflation is in free fall. Unemployment is remarkably low and the job market in general is robust. Real wages are rising.

At the same time, the discombobulated behavior has eased: quit rates, goods buying, stay at home behavior.

The irritant was COVID, the psychological impacts on society, and the follow on actions taken and by government institutions to correct course.

We see this in all of the data presented below but also, finally, in sentiment.

No, things aren't as bad as they seem in a vacuum, but our health (mental and physical) has to heal from the pandemic itself.

The further we get from the irritant the less irritated we will be.

It's this period, the "after this" period where investors should be looking.

And lastly, have patience with yourself. The irritant is fading, now is time to receive that reality.

The trauma is ending. Now care for yourself and others.

Now, here we go deeper into the data.

Preface

The United States has seen tremendous disinflation and that is echoed by the same type of price behavior in the UK and Euro Zone and dozens of other countries.

China is in outright deflation (negative inflation) and its PPI (wholesale prices) has been negative on a YoY measure for 14-straight months.

First, here is a chart of US PCE Price Inflation YoY (Source). We are now at 2.6%, down from a high of 7.1% in June 2022. The Fed’s target is 2.0%

Second, here is a chart of Core PCE Price Inflation YoY (Source). This is the Fed’s preferred measure of inflation as it excludes food and energy (like oil).

We are now at 3.1%, down from a high of 5.5% in Sep 2022. The Fed’s target is 2.0%

But the story is better than even that.

Six-month Core PCE is at 1.87%, below the Fed’s target and in contrast to the 4% inflation level in the first six-months of 2023.

But the magic in the United States takes these inflation trends and couples it with historically low unemployment, massive job gains, and dropping quit rate.

It’s not even Goldilocks, it’s Goldilocks squared… for now.

In order for the US to achieve its soft landing - and end to inflation while avoiding a recession - this was the path that was needed.

But there is risk.

The risk is that the trajectory that was so badly needed, a cooling of boiling economic data, doesn’t stop right where we want it to. That’s the risk, not a matter of fact.

That’s the trick with economic data, once data are in a trajectory it isn’t clear where it stops… until after it does.

But, for now, this is one of the most inconceivably good economic outcomes that could have been dreamed up: A booming GDP, booming employment, growing real wages, and plummeting inflation.

With data out earlier this week we also learned that the United States is producing more oil than any country in history… as in ever, for the month of November and it held that same distinction for October as well.

We can say, as of today, and it’s just a moment in time, that the inflationistas were dead wrong - embarrassingly so.

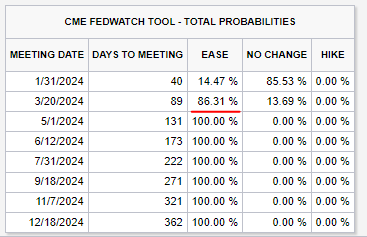

The futures’ market now reflects an 86% chance of a rate cut by the March FOMC (Federal open Market Committee) meeting:

And if you look at the right hand side of that table, the odds of a rate hike are zero - for any month.

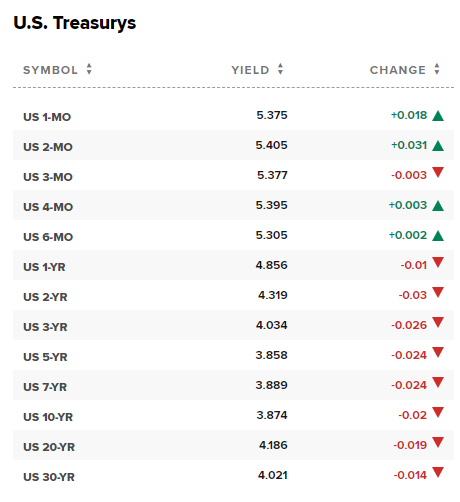

Yields are down slightly on the day:

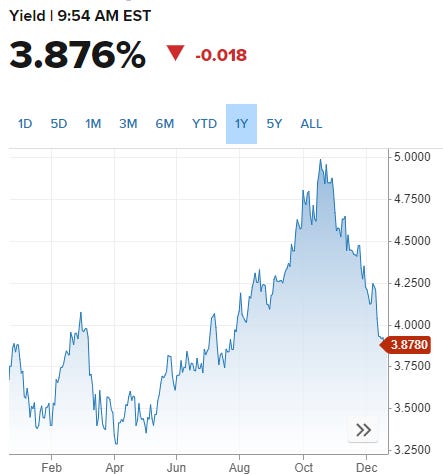

But the real move in yields is not about today.

Here is a chart of the yield on the 10-year treasury note: a massive recalibration.

The 10-year yield is the anchor for credit card rates, mortgage rates, and valuation discount rates. This one really matters.

It’s a fair question to ask: is the yield plummeting because inflation is dropping and it reflects the Fed cutting rates or… is it a reflection of a fear of recession and this is flight to safety?

Time will tell, friends, but for now, at this moment (and moments change) I’ll stick with the phrase I led with:

This is one of the most inconceivably good economic outcomes that could have been dreamed up.

So… Where do we go from here?

Well, if you’re a reader of my research then you know where I think we go from here.

We were clear on the CML Pro webinar on 4-1-2023 that we had this idea – this “after this” idea, and it went like this:

While there have been and are no shortage of opinions on the current time, there is a rather dearth of attention being paid to the “after this:”

A period where rates will drop, inflation will be lower, the focus will be on companies not countries, and the winners and losers will have been decided in this muck – which companies are gaining market share and which are not.

The revelation is not that we were in a high inflationary period and are in a recession risk period.

The revelation is that the winners (and losers) are being determined in those that have the ability (and desire) to look “after this.”

We dedicated substantial time to the impact of large language models (LLMs) like ChatGPT on the tech landscape and those “predictions” are already coming to bear.

We have named 9 as “after this” winners and YTD they are up 74%.

You can rad about CML Pro here:

Conclusion

This period is a wonder - a series of inconceivable data that, for a moment, are more than good, they are exceptionally good. But, don’t get slap happy.

Take the good as good. Then recalibrate and think about the future.

If you enjoy these posts and want deeper economic analysis and then the meat on the bone: a stock research service with Top Picks and performance double verified by an audit firm and then a hedge fund tracking firm, check out CML Pro.

For about a dollar a day you’ll have great access to company CEOs, expert channel checks, economic research, and our Top Picks list. That price is going rise by 2-fold in 2024 (inflation is real).

Now is the time to look at the “after this” period. That is, not just now, next month, and the month after that, but after the inflationary irritant is removed and after the potential recession that follows it; after this.

We have named nine “after this” winners thus far and the portfolio is up 74% YTD.

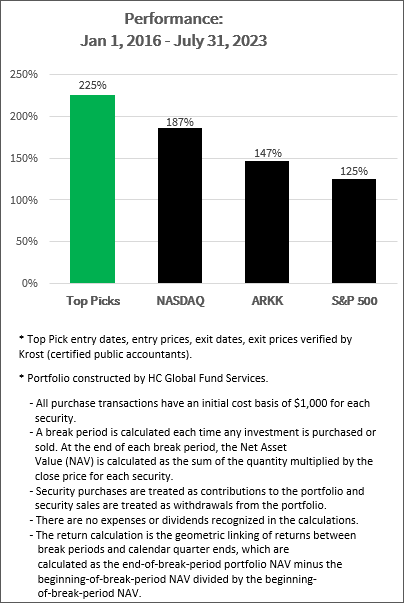

From January 1, 2016 through June 31, 2023 (more than 7.5 years) this how our tracking portfolio has done relative to other benchmarks:

Jan 1, 2016 - Jun 31, 2023

We have an eye toward the “after this” period and have named nine after this winners.

Get access to those nine names and all of our research and our community at CML Pro here.

Legal

The information contained on this site is provided for general informational purposes, as a convenience to the readers. The materials are not a substitute for obtaining professional advice from a qualified person, firm or corporation. Consult the appropriate professional advisor for more complete and current information. Capital Market Laboratories (“The Company”) does not engage in rendering any legal or professional services by placing these general informational materials on this website.

The Company specifically disclaims any liability, whether based in contract, tort, strict liability or otherwise, for any direct, indirect, incidental, consequential, or special damages arising out of or in any way connected with access to or use of the site, even if I have been advised of the possibility of such damages, including liability in connection with mistakes or omissions in, or delays in transmission of, information to or from the user, interruptions in telecommunications connections to the site or viruses.

The Company makes no representations or warranties about the accuracy or completeness of the information contained on this website. Any links provided to other server sites are offered as a matter of convenience and in no way are meant to imply that The Company endorses, sponsors, promotes or is affiliated with the owners of or participants in those sites, or endorse any information contained on those sites, unless expressly stated.