Housing Is Getting Built; A Remarkable Finding in Finance

Housing Is Getting Built; A Remarkable Finding in Finance

Preface

Today we focus on data that surrounds permits for housing and the number of housing starts and then share a remarkable finding we just came across.

Economic data first…

Building permits came in above estimates after a lackluster prior two months.

(Building Permits refer to the approvals given by a local jurisdictions before the construction of a new or existing building can legally occur.)

Permits reached the highest level since October 2022; however, they remained 12.7 percent below the level recorded in May of the previous year.

The month over month gain of 5.2% came in far stronger than the consensus estimate of a 0.6% rise.

Housing starts roared higher, coming in well above consensus estimates, surging 21.7% month-over-month to reach a seasonally adjusted annualized pace of 1.631 million in May 2023. The consensus estimate was for a 0.1% drop.

This marked the highest level since April of 2022.

Multi-family housing starts are near a 30-year high.

This sure feels like a stabilization within the housing market.

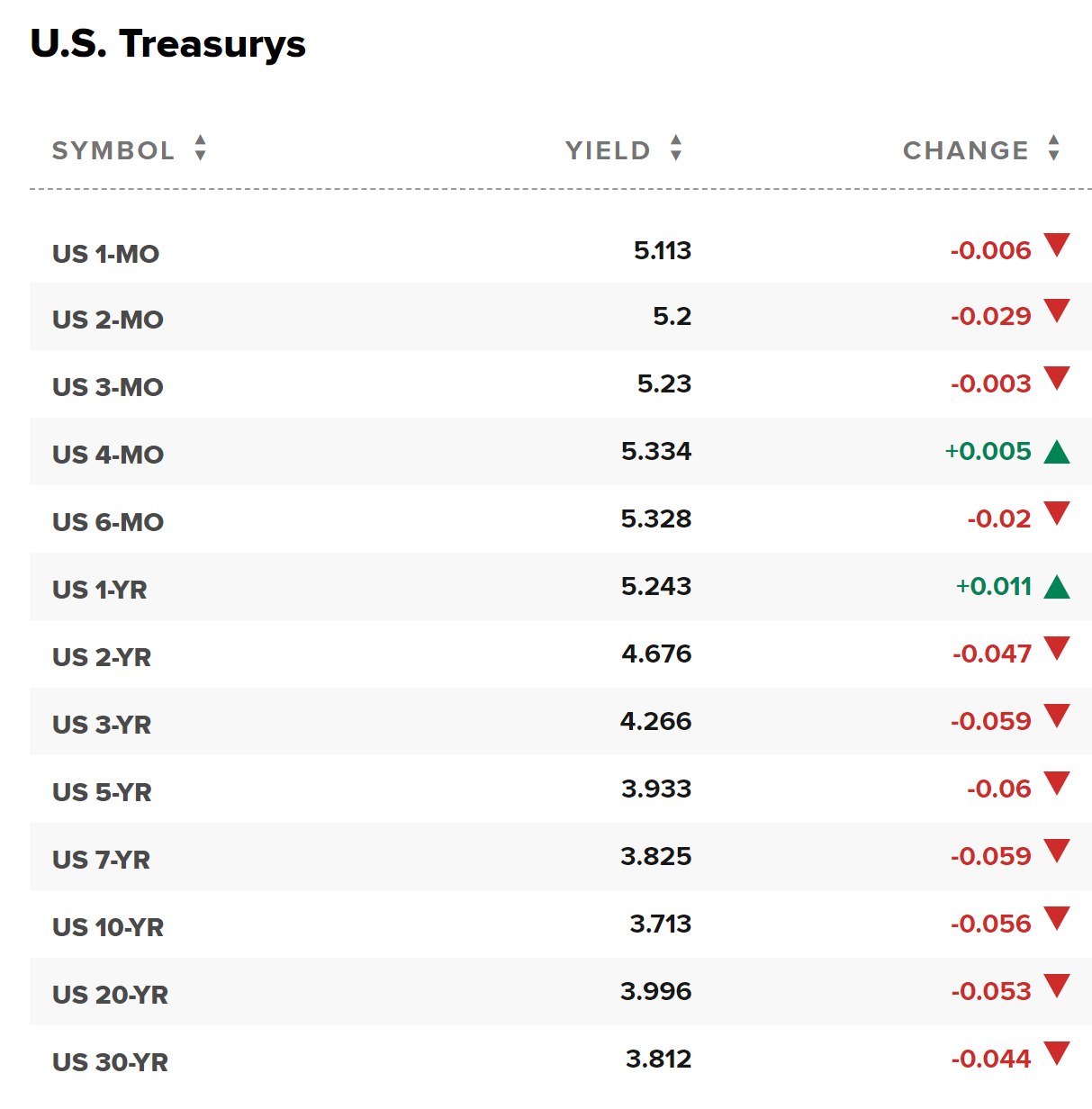

Treasury rates are slightly lower this morning in the early trade:

The odds of a rate hike in the next FOMC meeting are now at 72%.

Remarkable Finding

We have some exciting news from our laboratory:

We have a remarkable finding that is, from our perspective, the first distinguishable edge discovered using ChatGPT / LLMs + domain expertise / internal machine learning in finance.

With virtually 100% confidence, we can claim we found an aberration in finance.

This would be the second of my 25 year career. (the first was published in an academic journal and became the backbone of the hedge fund Governance Investors before the company that owned the algorithm was purchased by Morgan Stanley Capital International (MSCI).

We found that selling a put spread in stocks that have certain proprietary kurtosis (tail) dynamics versus doing same without, has a higher win rate with 99.9998% statistical significance over 1/2 a year…

… It has 99.9999999997% significance at 3 yrs for win rate and 100% (at 20 decimals points) over 5 yrs for win rate.

This is over 35,600 backtests for S&P 500 constituents.

That's the opening salvo.

The results for stock investors are equally as remarkable, with a 98.5% statistical significance comparing the win rate for a basket of stocks with the kurtosis dynamics versus those without over 5-years using the constituents of the S&P 500 and return outperformance with it.

(These are significance numbers, not the actual win rates - nobody has a 99% win rate; that's tomfoolery to make such a claim.)

We look forward to seeing you there.

Stock and option investors will be met with rather stunning results and implications for trading.

We will be sharing this research and giving access to using it for stock and option trading in our webinar (which is free) scheduled for June 29th.

You can register for the webinar here:

Turning AI, ChatGPT, and LLMs into Profits - A Remarkable Finding

Alright, more economic data below.

Keep reading with a 7-day free trial

Subscribe to Daily Economics to keep reading this post and get 7 days of free access to the full post archives.